Value Partners SA and VP Services are members of the OEC (Ordre des Experts Comptables) of Luxembourg, itself a member of IFAC.

VPsf is supervised by the CSSF (Commission de Surveillance du Secteur Financier), Luxembourg’s financial regulator.

Overview

Our Services

Value Partners S.A. and VP Services are members of the OEC (Ordre des Experts Comptables) of Luxembourg, itself a member of IFAC.

VPsf is supervised by the CSSF (Commission de Surveillance du Secteur Financier), Luxembourg’s financial regulator.

Overview

Our Services

Value Partners S.A. and VP Services are members of the OEC (Ordre des Experts Comptables) of Luxembourg, itself a member of IFAC.

VPsf is supervised by the CSSF (Commission de Surveillance du Secteur Financier), Luxembourg’s financial regulator.

Overview

© 07.2025 • Value Partners • All rights reserved

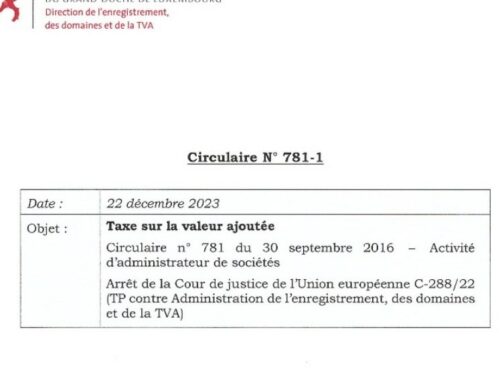

On 13 July 2023, the European Court of Justice (ECJ) released the opinion of the Advocate General in the pending case having the aim to determine if a director, member of a board of Directors, is to be considered as a VAT taxable person.

Two questions were referred to the ECJ:

1/ The first question was to determine if a natural person, who is a member of the board of directors of a public limited company incorporated under Luxembourg law can be considered as carrying out his or her activity “independently”?

The opinion of the Advocate General released yesterday by the ECJ is to consider as criteria, in the context of the necessary overall assessment, the fact that the person concerned, as a typical taxable person does, bears an economic risk personally and acts on his own economic initiative to be considered as carrying out an economic activity independently.

2/ The second question was to determine if a natural person, who is a member of the board of directors of a public limited company incorporated under Luxembourg law and remunerated for that activity, is carrying out an “economic” activity within the meaning of the EU VAT Directive 2006/112/EC.

On that second question, the Advocate General proposes to the ECJ to reply that it follows from the principle of neutrality of legal form that a natural person who is a member of a body of a company which is required by law and who receives remuneration for that activity as a member of that body cannot in this respect be regarded as carrying out an independent economic activity.

Should you require further information, please reach out to Steve Georges.

Find our more about our VAT services here.